By Amy Killelea and JoAnn Volk

The 2025 Affordable Care Act (ACA) open enrollment period has been a difficult one, as Marketplace enrollees are facing significant premium hikes for 2026 coverage. When Marketplace coverage—which has to meet ACA standards for benefits, non-discrimination, and network adequacy—becomes tougher to afford, non-ACA compliant products (sometimes referred to as “junk plans” because of the lack of state and federal protections) may gain traction, especially when they are marketed as cheap alternatives to the Marketplace and the federal government has relaxed enforcement.

These non-ACA compliant products can be harmful in three ways: because they are not subject to most state and federal health insurance standards, they often come with major coverage limitations, including skimpy benefits and an array of exclusions; these products are often misleadingly marketed as alternatives to ACA Marketplace coverage but the products being sold are not major medical coverage at all, creating a false and confusing comparison; and these non-ACA products are often marketed toward relatively healthy individuals, siphoning off these populations from the individual market and exacerbating the affordability issues in that market.

State policy makers can curb the availability of these products or put guardrails and protections around them through legislation or regulation. In the immediate term, though, state insurance regulators can ramp up oversight of these non-ACA compliant products and more aggressively monitor deceptive marketing practices. As the marketing of non-ACA compliant products grows, consumers who end up in a plan that was “too good to be true” can face significant financial harm.

What Are “Junk Plans”?

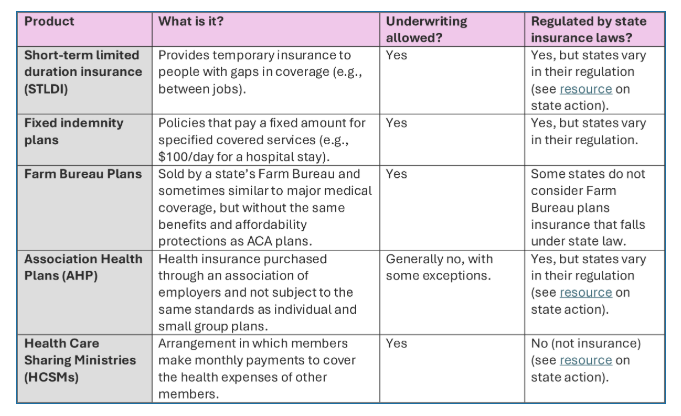

The term “junk plans” is a catch-all meant to capture a range of products that do not have to comply with ACA protections such as benefits requirements and non-discrimination provisions. Many of these products deploy medical underwriting, which allows insurers to base the availability and price of a plan on an individual’s health status. This can make these products more attractive to younger people without preexisting conditions. Exhibit 1 lists types of junk plans.

Exhibit 1: Types Of Junk Plans

Source: Authors’ creation.

How Does Misleading Marketing Of Junk Plans Impact Consumers?

Many of the non-ACA-regulated products described above are not meant to replace major medical insurance. A fixed indemnity plan, for instance, provides what is essentially an income replacement benefit when someone is hospitalized, which can serve as an extra layer of financial protection when paired with a major medical insurance plan. The problem arises when these non-ACA regulated products are marketed as alternatives to major medical insurance. Propping up a substandard product as just another insurance plan choice in a dizzying array of options creates an apples to oranges comparison, with consumers thinking they’ve found a cheap alternative that ends up too good to be true.

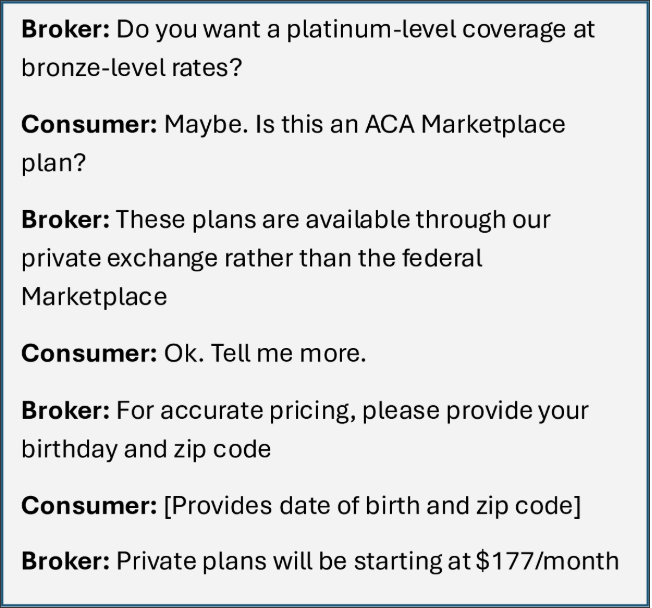

Take the example from a broker marketing text exchange with one of the authors, described in exhibit 2.

Exhibit 2: Text exchange with broker

Source: Authors’ transcript.

The implication is that the broker is selling a product on a “private exchange” that may be an alternative to ACA Marketplace coverage (the Marketplace is also sometimes referred to as an exchange, adding, likely intentionally, to the confusion). However, a call with this broker revealed that the products available on this private exchange are fixed indemnity plans. The broker noted that unlike a Marketplace plan, the private plan has no deductible or copayments, instead it provides “first dollar coverage” (meaning the insurer begins payment as soon as an insurable event occurs without requiring a patient to meet a deductible or pay out of pocket at the point of sale) and is available at a premium hundreds of dollars lower than Marketplace plans. While it is true that a fixed indemnity plan typically does not come with copayments or deductibles, this isn’t because a consumer has found the deal of a lifetime. It’s because the product is not designed like an insurance plan at all. With a fixed indemnity plan, consumers may pay nothing when they receive care, only to be saddled with a bill later when they learn the plan’s fixed dollar payment for the service received does not come close to covering the full cost, leaving the consumer responsible for the balance.

Multiple studies have documented misleading marketing being used to lure consumers shopping for coverage into non-ACA regulated products. A 2019 Georgetown CHIR study found that short-term plans were often marketed as cheaper alternatives to “Obamacare” plans, leaving consumers confused as to how short-term plans were different from Marketplace plans. A similar 2020 analysis from the Brookings Institution and another from CHIR found that misleading marketing may have been even more pronounced during the COVID-19 pandemic as uninsured consumers struggled to find coverage options amid widespread unemployment. A Government Accounting Office study published in 2020 conducted covert testing of marketing practices for select non-ACA compliant products and found that in a quarter of their covert calls “sales representatives engaged in potentially deceptive marketing practices … by omitting or misrepresenting information about the products they were selling.” More recently, CHIR researchers found brokers using misleading marketing to steer low-income consumers losing Medicaid to limited benefit plans.

What Are State Regulators Doing About Junk Plans?

While misleading marketing of non-ACA compliant plans is not new, it may be a more pronounced problem during an open enrollment period when consumers are facing large Marketplace premium hikes. There are two routes that states can take to protect consumers, and their insurance markets, from the harms associated with these types of products. First, states can place guardrails around the products themselves, in some cases prohibiting their sale altogether or putting conditions on their sale.

Second, states can tamp down on misleading marketing of non-ACA compliant products. State insurance regulators have primary authority over the regulation of insurance, including licensure and oversight of insurance brokers. Some states require specific consumer “black box” warnings on these products, requiring carriers to disclose clearly that the product is not compliant with the ACA and in some cases how the product differs from ACA coverage. State insurance departments—including Colorado, Maryland, and Texas—have issued guidance for consumers on how to tell Marketplace coverage from non-ACA compliant products. New Mexico issued guidance putting insurers and brokers on notice that deceptive and misleading marketing is illegal under state consumer protection laws.

Not all non-ACA-compliant plans are inherently harmful to consumers, but when they are marketed as cheap alternatives to major medical coverage, consumers can find themselves enrolled in products that don’t actually provide the financial protection they thought they were getting. The Trump administration is moving forward with a proposed regulatory agenda that includes expanding access to non-ACA compliant products and even incentivizing states to deregulate these plans. States, however, have a great deal of regulatory authority over many of these products, as a new report from Blood Cancer United points out. States may consider implementing additional guardrails and heightened oversight to ensure consumers don’t end up underinsured or in substandard products they thought were major medical plans.

Amy Killelea and JoAnn Volk “The Peddling Of “Junk Plans” To Consumers Facing Higher Insurance Premiums” January 16th, 2026, https://www.healthaffairs.org/content/forefront/peddling-junk-plans-consumers-facing-higher-insurance-premiums. Copyright © 2026 Health Affairs by Project HOPE – The People-to-People Health Foundation, Inc.