Site-Neutral Payment Reform and the Commercial Market

A policymaker’s guide to exploring site-neutral payment for outpatient services in the commercial health insurance market

Introduction

Commercial site-neutral payment policies establish the same payment rate for all care settings, usually by specifying or capping the total amount a health care provider charges and/or a payer pays for specified outpatient services. These reforms can make health care more affordable. However, policymakers have a number of options for designing these policies, which affect their implementation and impact.

This resource guides you through four decision domains that will shape your site-neutral payment policy, including different options and considerations for each:

Curious About Medicare?

Among major health insurance programs, only Medicare uses site-neutral payments, and only in limited circumstances. Explore our resource “What You Need to Know About Medicare Site-Neutral Payment Reform” for more information.

Getting Started

In this section, you’ll learn what commercial site-neutral reforms are, why reforms are needed and their potential impact.

What Is Site-Neutral Payment?

In our current health system, payment rates for health care services can differ based on where care is provided. Hospitals or health systems can capitalize on these differences to generate higher revenues without measurable improvements in care quality compared to other settings. These site-based differences generally are more extreme in the commercial health insurance market than in public programs.

In contrast, a site-neutral approach ensures reimbursement for a given service is similar or the same regardless of whether the patient receives care in a hospital-owned setting or an independent doctor’s office or surgery center. Such policies are grounded in the belief that payments should reflect the resources health care professionals need to provide care in the most-efficient, lowest-price setting that is safe and clinically appropriate for that service.

Why Reforms Are Needed

Care provided in hospital outpatient departments (HOPDs) is one of the fastest growing components of health care spending, driven by the disproportionately high prices HOPDs command from commercial payers in combination with growing use of outpatient settings. Other outpatient settings—such as freestanding physician offices and ambulatory surgical centers (ASCs)—charge commercial payers lower rates for the same services but have not experienced growth in prices or volume comparable to HOPDs.

[[ACCORDION START: Why Is Use of Hospital-Based Outpatient Care Growing?]]

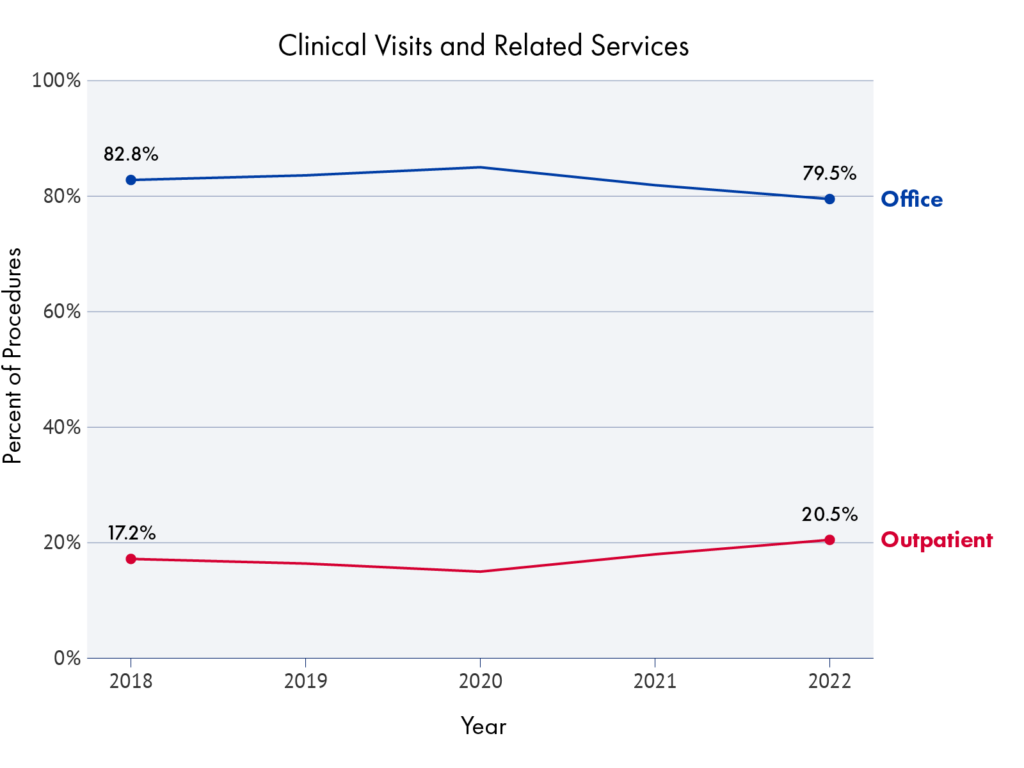

Over the past few decades, hospital outpatient utilization has grown significantly as has outpatient revenue as a share of total hospital revenue. This shift is driven in part by medical advancements that have allowed surgeries and other procedures traditionally performed on an inpatient basis to move to less-intensive settings. At the same time, hospitals and health systems have steadily acquired physician practices, meaning that care that was once delivered outside of a hospital system may now be performed in settings that hospitals own and license as HOPDs. For some services, like clinic visits, the site of care has demonstrably shifted from freestanding offices to HOPDs.

Figure 1.

Shift in Setting for Clinic Visits in the Commercial Market, 2018–2022

[[ACCORDION END]]

[[ACCORDION START: How Much Higher Are Hospital Charges for Outpatient Care?]]

Care provided in an HOPD is generally more expensive than care provided in freestanding physician offices and (ASCs). These site-based payment differences are especially wide in the commercial market and can be particularly notable for certain services, such as clinic visits, diagnostic testing, and drug administration. For these services, HOPDs may charge three times as much, or more, than office-based providers In many cases, reimbursement between these settings is diverging further as outpatient facility fee increases consistently outpace professional fee increases. The variation in commercial payments across settings can be traced to hospital billing practices and contract negotiations between payers and providers.

Figure 2.

Average Prices Paid by Setting for Selected Services in the Commercial Market, 2018–2022

[[ACCORDION END]]

[[ACCORDION START: Why Are Hospital Charges Higher for Outpatient Care?]]

The ability for HOPDs to charge a facility fee for outpatient care and market power gained through consolidation both contribute to higher payments for HOPDs:

Split Billing: HOPDs and the clinicians working there usually issue two separate bills for the same service, a practice known as split billing. The hospital charges both a professional fee, which seeks payment for the treating clinician’s time and labor, and a facility fee, which is meant to cover the facility’s overhead costs. In contrast, a freestanding physician office will charge a single professional fee that covers the clinician’s time and labor plus office overhead. The facility fee is generally much larger than the overhead portion of a freestanding physician’s bill. This higher overhead charge may reflect higher costs directly related to delivering services in an HOPD, but it may also reflect the facility’s allocation of other operating costs across hospital departments. Split-billing in the commercial market derives from Medicare, which reimburses hospitals and physicians under separate payment systems—the Outpatient Prospective Payment System (OPPS) and Physician Fee Schedule, respectively.

Figure 3.

Average Spending by Total and Component Parts at Physician Offices Compared to HOPDs for Primary Care Office and Pediatric Wellness Visits in the Commercial Market, 2022

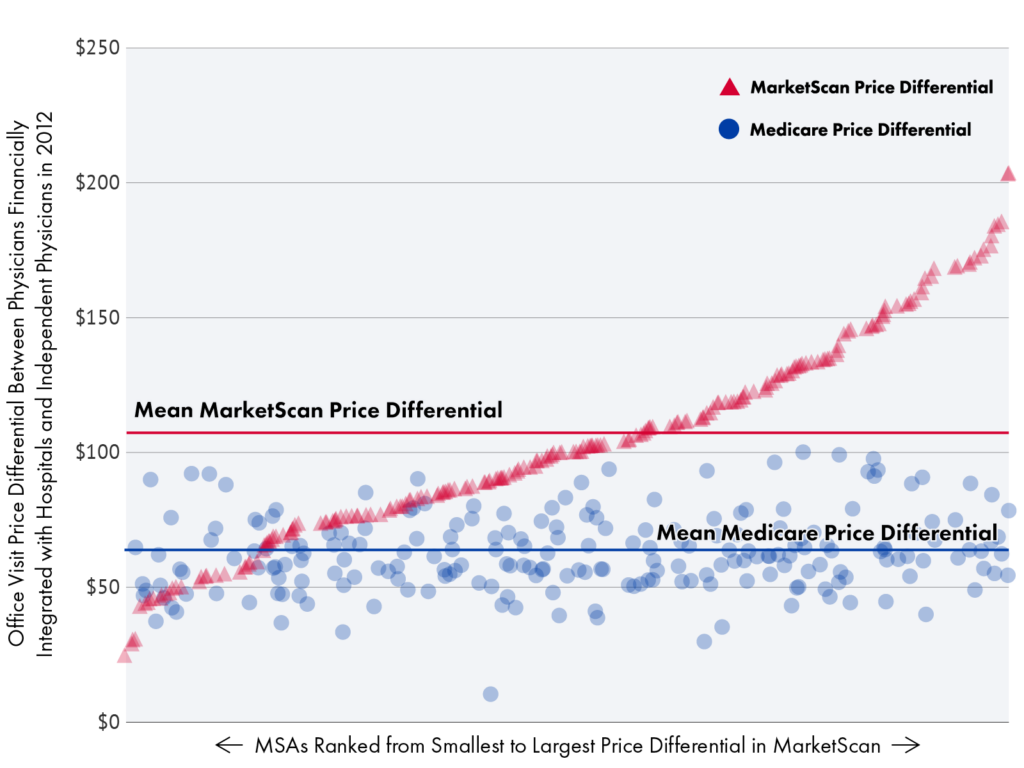

Provider Consolidation: Health care provider consolidation and the negotiating power consolidation conveys exacerbates these price differences in commercial markets. Ample research shows that hospital prices are higher in consolidated hospital markets, even when the payer market is also consolidated. Vertical integration between hospitals and other types of providers also gives health systems greater leverage in contract negotiations with payers and increases prices. The potential for higher rates then create further incentive for consolidation and integration in a self-reinforcing cycle. The role market power can play in site-of-service differences can be demonstrated by comparing site-based price differences in Medicare and the commercial market. Medicare reimbursement rates are based on expected provider costs, not on providers’ relative market power. In the commercial market, by contrast, providers and payers negotiate payment rates, which vary significantly based on providers’ market power and other factors. While Medicare pays more when care is provided in a hospital setting compared to a freestanding setting for most services, the site-based payment differences in Medicare within the same geographic area are relatively smaller than those in the commercial market.

Figure 4.

Difference in Mean Prices for Office Visits Between Independent and Hospital-Integrated Physicians, by Metropolitan Statistical Area (MSA) for Medicare and MarketScan Populations

[[ACCORDION END]]

[[ACCORDION START: How Do Hospitals Justify Higher Charges?]]

Hospitals sometimes justify higher charges for hospital-based outpatient care by citing:

- Higher operational costs and their ability to provide more specialized care than a freestanding setting, such as a physician’s office or ASCs.

- Unique costs, such as emergency departments, stand-by capacity, and trauma care. Higher HOPD prices provide indirect subsidies for other critical services that only hospitals can provide to the community.

- HOPDs serve more complex patients than those in freestanding settings.

These explanations, however, offer an incomplete picture because:

- Many outpatient procedures can safely be provided to most people in lower-price, non-hospital-based settings. For example, the Massachusetts Health Policy Commission determined that nearly half of the services delivered in hospital HOPDs in 2019 and 2022 could have been safely provided in a lower-cost setting, while the Medicare Payment Advisory Commission (MedPAC) has identified an illustrative list of 66 service categories, known as Ambulatory Payment Classifications, that are regularly delivered in HOPDs but are most often provided in freestanding physician offices or ASCs under Medicare.

- As MedPAC has noted,using higher HOPD prices to cross-subsidize other care distorts prices, leading to payments that are too high for HOPD care and too low for other services. Overpaying for outpatient care at hospitals also fails to target resources where they are most needed within the hospital, and encourages hospitals to acquire physician practices.

- Evidence on case-mix severity is mixed, and differences in patient care can be addressed more directly. One study found that patients receiving care at an HOPD had poorer health, based on past diagnoses and health expenditures, than patients receiving the same service in a freestanding physician office, and the HOPD patients also received more additional services. Researchers acknowledged that this could be driven by more comprehensive coding or upcoding, however. In contrast, at least for the 66 service categories it identified, MedPAC found only small differences in patient severity between hospital and freestanding settings, and that these differences did not have a significant effect on hospital charges. Either way, however, actual differences in the complexity of a specific patient or the care provided to them can be addressed directly by billing a higher service level or for the additional services provided, rather than by maintaining different payment rates for the same service in different settings.

[[ACCORDION END]]

Savings

Recent cost-estimates suggest that site-neutral payment reforms for commercially insured outpatient services could meaningfully reduce health spending and offer one avenue for protecting consumers from high out-of-pocket cost-sharing and premium increases.

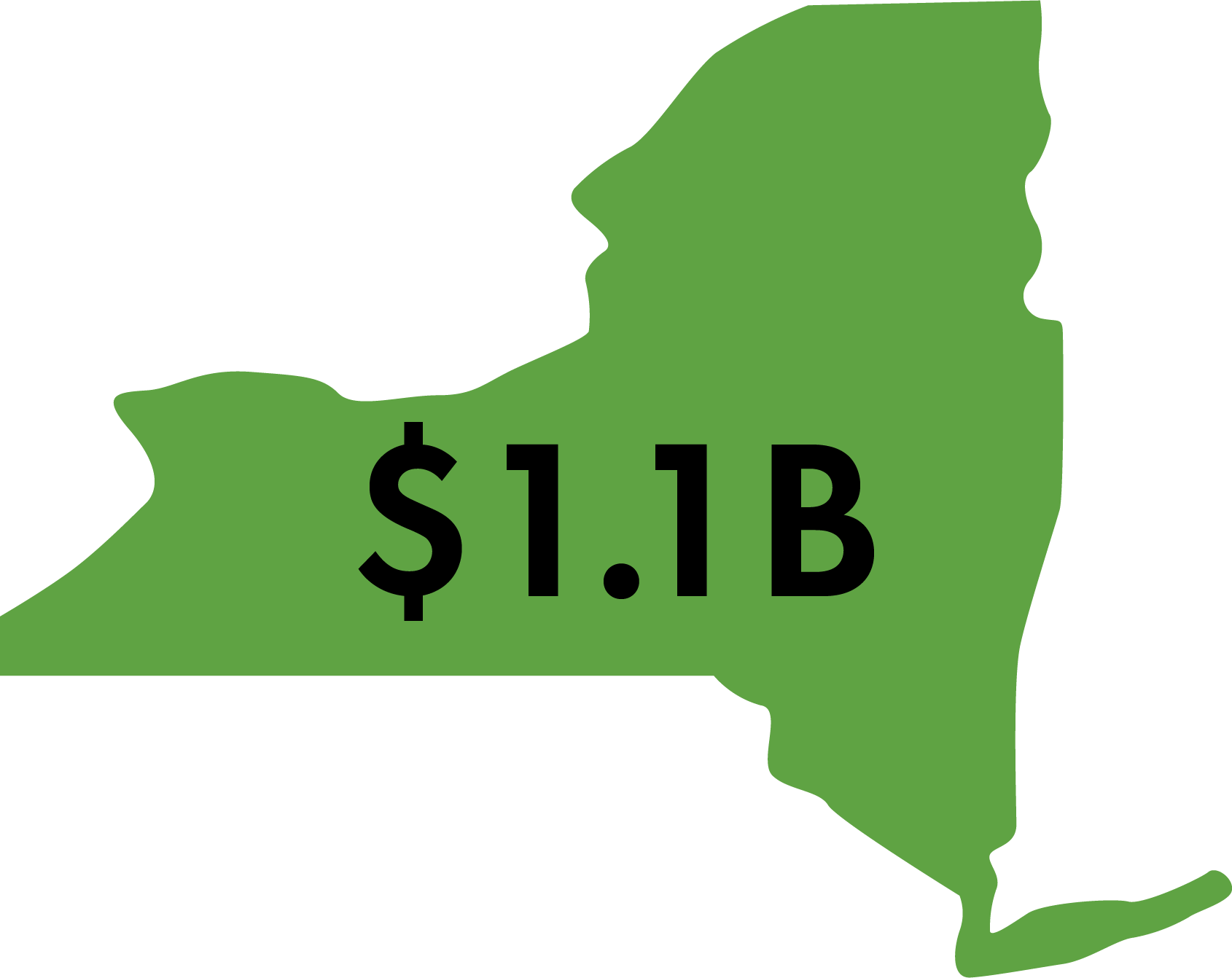

[[ACCORDION START: State-Level Estimates]]

The New York Fair Pricing Act is one of several state-level proposals that apply site-neutral payment for outpatient care in the commercial market. According to one analysis, it would, if enacted, yield annual statewide savings of $1.1 billion in 2022 dollars. This proposal establishes a cap on commercial payments for all care settings equal to 150 percent of Medicare’s non-hospital payment—either the physician fee schedule (PFS) or the ASC rate, depending on the service in question—for a defined set of outpatient services similar in scope to those identified by MedPAC. The proposal would also prohibit facility fee payments for services delivered in HOPDs.

Figure 5.

Potential One-Year Total Savings from MedPAC-style Site-Neutral Reforms in the Commercial Market, New York, 2022 Dollars

| |

|---|---|

| Reach | New York State |

| Scope | On/Off-campus: MedPAC-identified services |

| Pricing Approach | 150% Medicare rates |

[[ACCORDION END]]

[[ACCORDION START: National-Level Estimates]]

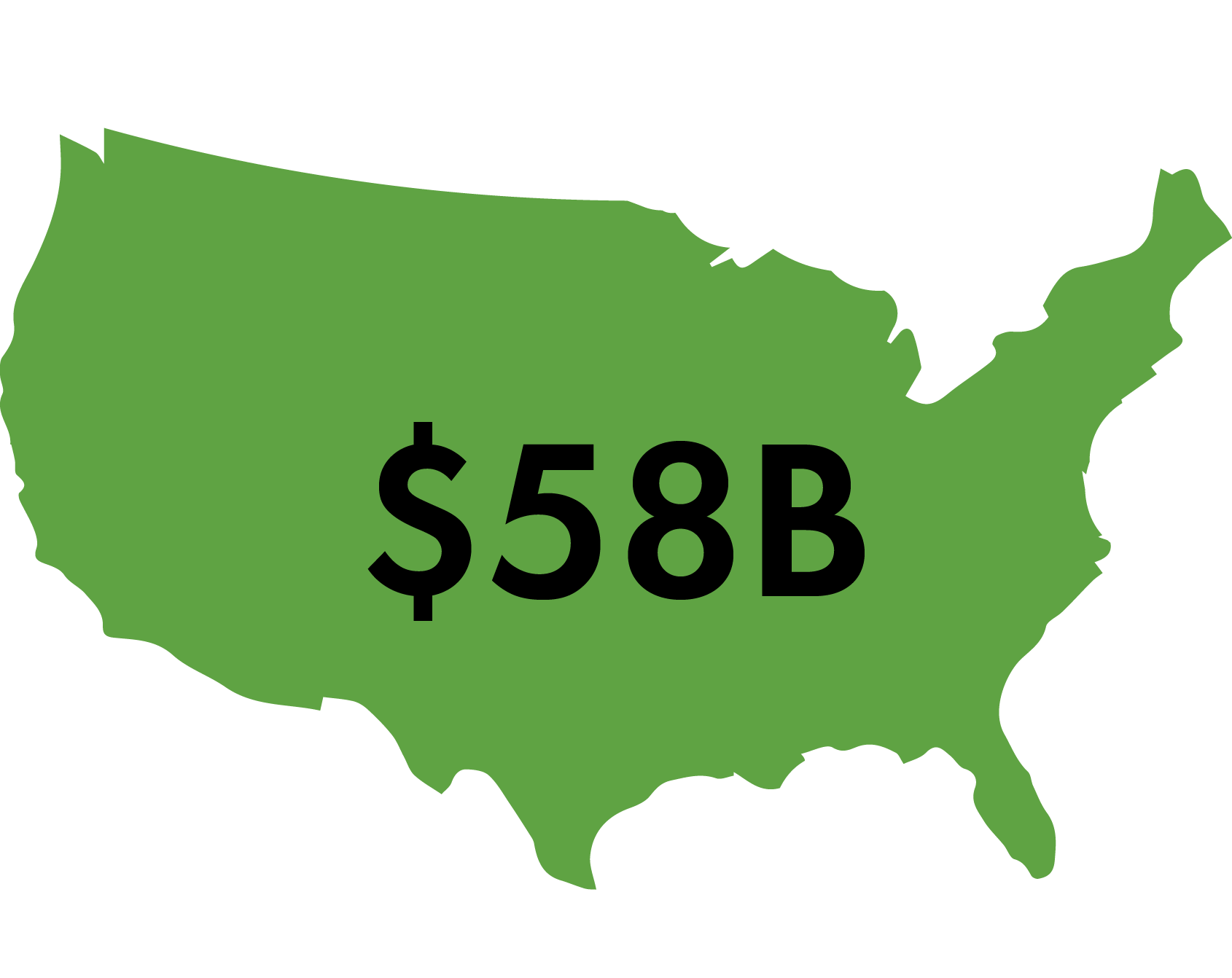

National-level proposals show even more significant savings. One microsimulation model concluded that nationwide implementation of site-neutral payment in the commercial market, based on the MedPAC-identified service categories, would result in $58 billion in savings in 2022. Ten-year savings, from 2024–2033, would total $898 billion, leading to premiums for employer-sponsored health insurance that would be 5 percent lower than in the absence of these savings.

Similarly, the Committee for a Responsible Federal Budget (CRFB) estimated potential cost-savings for a three-pronged commercial site-neutral payment proposal: (1) a prohibition on split billing for services delivered in off-campus HOPDs; (2) a payment cap for services delivered at an HOPD tied to the median payment for the same service when provided in a physician office; and (3) a further payment cap for low-complexity services delivered in on-campus HOPDs. The CRFB estimated that this combination would reduce national health expenditures by $458 billion over ten years through a combination of lower premiums and patient cost-sharing. Additional effects would include reduced federal spending on Marketplace premium subsidies, increased tax revenues from higher taxable wages, and related reduced interest payments on the national debt, resulting in $117 billion in federal deficit reduction.

Figure 6.

Potential One-Year Total Savings from MedPAC-style Site-Neutral Reforms in the Commercial Market, Nationwide, 2022 Dollars

| |

|---|---|

| Reach | United States |

| Scope | On/Off-campus: MedPAC-identified services |

| Pricing Approach | Commercial median rates |

[[ACCORDION END]]

[[ACCORDION START: How Consumers Save]]

Current pricing practices have resulted in higher costs for patients and health insurance enrollees for outpatient care. Depending on their insurance benefit design, patients can incur cost-sharing responsibility for not only their unmet deductible, if applicable, but also both the professional fee (typically a copayment) and the facility fee (often co-insurance). One study found that patient cost-sharing is 200 percent higher for elective procedures performed in an HOPD compared to procedures performed in physician offices. Similarly, vertical integration and the resulting shift to outpatient care have been associated with significant increases in individual market premiums.

Site-neutral payment approaches that permit only a single bill for an outpatient service, regardless of setting, insulate consumers from responsibility for two cost-sharing payments. Similarly, site-neutral payment requirements that base payment on the lowest-cost and most-efficient, safe, and appropriate setting will reduce outpatient spending and, in turn, coinsurance and deductible payments as well as health insurance premiums.

The CRFB estimated that its three-part site-neutrality proposal would reduce premiums by $386 billion over ten years while reducing consumers’ cost-sharing responsibilities by $73 billion over the same timeframe.

Consumer out-of-pocket savings under the New York Fair Pricing Act are estimated to range between $168.9 million to $213.4 million a year in 2022 dollars.

[[ACCORDION END]]

Other Benefits

Site-neutral payment methodologies can help correct the market distortions created by current payment practices in the following ways.

[[ACCORDION START: Equitable Payment]]

Site-neutral payment ensures that health professionals and institutional providers receive a payment—and the same payment—that reflects the clinical expertise and actual resources a service requires in the most efficient setting.

[[ACCORDION END]]

[[ACCORDION START: Reduced Market Power]]

By reducing payments to institutionally affiliated providers, site-neutrality also reduces financial incentives for further vertical integration and could therefore limit the additional market leverage that highly integrated hospital systems acquire and wield in contract negotiations.

[[ACCORDION END]]

Tradeoffs

Adoption of site neutral payments could lead to the following changes in behavior by health care providers:

[[ACCORDION START: Changes in Utilization, Access, and/or Quality]]

There is strong research evidence that health care providers can and do become more efficient when faced with reduced payment rates, and that there is little correlation between provider prices and quality of care. Nonetheless, policymakers should approach cost containment aware of the multidimensional nature of health care spending. For example, hospitals could try to make up revenue by increasing utilization, including potentially inappropriate utilization, or patients could experience reduced access to services or lower health care quality. These risks do not necessarily warrant inaction—ever accelerating spending growth also imperils access to affordable, necessary care—but suggest complementing any reform with ongoing data collection and monitoring and maintaining flexibility in policy design to adapt to changing circumstances.

[[ACCORDION END]]

[[ACCORDION START: Revenue Shifting]]

There will be a risk that some hospitals and health systems may make up for lost revenue by raising prices for other service lines. This risk decreases with broader reforms, as the hospitals and health systems have fewer services and settings available to shift costs too. Policymakers should weigh whether it is politically or administratively feasible to undertake more expansive commercial price regulation that minimizes the risk of price shifting, or if this risk is acceptable given other potential benefits—such as reducing consumer out-of-pocket costs for key services and rationalizing some commercial prices—of a narrow policy change.

[[ACCORDION END]]

Policy Design

In this section, we’ll explore the four central domains you will need to address as you craft your site-neutral payment policy: scope, payments, operations and administration.

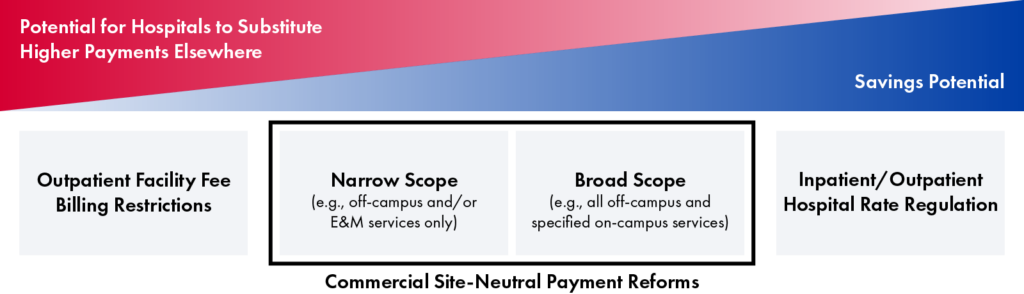

Scope

Policymakers will need to decide whether to apply the site-neutral payment policy to a narrow or broad set of outpatient services, settings and hospitals, and consider whether or not to include non-hospital providers.

Services & Settings

A commercial site neutral payment policy may apply to a narrow or broad set of outpatient services and settings.

- Narrow: A narrower scope of reforms will generate lower savings, both because of the more limited reach and because hospitals will have more options to make up lost revenue by increasing prices on unregulated services and settings. While policymakers making narrow reforms can specify the services or settings to which a policy applies in legislative language, policymakers drafting broader reforms may choose to defer some details to a regulatory process.

- Broad: If policymakers seek to regulate a more comprehensive set of services, they may want to look at how MedPAC has approached identifying services that may be suitable for site-neutral services in Medicare. MedPAC reasons that a service that is most commonly provided in a freestanding physician office or an ASC can be safely provided in that setting for most patients, and thus hospital payments could be aligned with the payment rate for that setting. MedPAC excludes some services from this approach, such as emergency and trauma care, and also advises policymakers to consult clinician perspectives as part of the policy design and implementation process.

Policymakers can review existing outpatient facility fee laws in the commercial market, as well as Medicare site-neutral payment reform proposals for ideas. Should policymakers choose to model commercial reforms on Medicare proposals, they may need to adjust for differences between the commercial and Medicare enrollee populations and differences in payment practices.

| Less Comprehensive | More Comprehensive | |

|---|---|---|

| Types of Services | Evaluation and management (E&M), preventive, and/or telehealth services only | All services that can be safely and appropriately provided in an independent setting |

| Location | Off-campus HOPDs only | Both on- and off-campus HOPDs* *Scope of services may vary between settings |

| Type of HOPD | Only specified HOPDs (e.g., clinics, laboratory, radiology and imaging departments) | All HOPDs unless exempted (e.g., emergency departments) |

Exemption Considerations

Policymakers may want to exempt certain types of HOPDs that have higher overhead costs, such as emergency departments. Such policies should be written carefully. In Medicare, for example, an exemption from site-neutral payments for dedicated emergency departments allows physician practices that newly affiliate with a hospital to locate inside off-campus emergency departments and maintain higher payment rates.

Types of Hospitals

Policymakers will need to consider whether they want to apply commercial site-neutral payment requirements to some or all hospitals, including:

- General acute care hospitals

- Specialty acute care hospitals, such as children’s hospitals and cancer hospitals

- Critical access hospitals

Policymakers may also want to design their policy to exempt certain hospitals or types of hospitals based on local considerations, or model exemptions off of current Medicare site-neutral policies. Alternatively, policymakers may use payment adjustments or phase-in options to protect financially vulnerable hospitals without resorting to permanent exemptions.

Figure 7.

Medicare Site-Neutral Requirements by Hospital Type

*Medicare makes up any shortfall between what these hospitals are set to be paid under the Outpatient Prospective Payment System (OPPS), to which site-neutral requirements apply, and what they would have received under the more generous cost-based methodology that preceded Medicare’s adoption of OPPS.

Other Providers

Policymakers will also need to determine whether to regulate payment rates for freestanding providers and settings, including physician practices and ASCs. Including these providers would ensure that payments are, in fact, site-neutral, but there is less precedent for regulating commercial payments for non-hospital providers.

Alternatively, a policy could set hospital payment rates at a level that approximates the current mean or median market rate for freestanding providers and settings, without directly regulating these providers. This potentially could open the door to gaming or unintended consequences in some markets, however, and would require close monitoring to ensure freestanding provider payment amounts remain at an appropriate level.

Payment

To ensure that a commercial site-neutral payment policy generates savings, policymakers need to create a methodology that puts specific bounds on what hospitals (and potentially other providers) can charge and updates these limitations over time.

Payment Level

The primary question facing policymakers is how high or low to set reimbursement for site-neutral services:

- Lowest Current Price: To maximize savings, policymakers may want all providers reimbursed at the amount paid to the lowest-price setting in the market. This setting will likely be freestanding physician offices and ASCs that have no hospital or health system affiliation. (Some physician offices or ASCs may be affiliated with a hospital, but continue to operate as freestanding facilities while benefiting from the hospital’s negotiating power to increase their reimbursement rates.)

- Adjusted Price: Alternatively, policymakers may aim somewhere above that if the amount is potentially inadequate to reasonably cover providers’ costs and maintain access and quality if applied market wide.

Regardless, policymakers likely will want to differentiate any site-neutral services that are more commonly or appropriately provided in an ASC, such as colonoscopies, rather than an office-setting. ASCs generally cost more than physician offices, but less than HOPDs. Prices for services most suited to delivery in an ASC should reflect the additional costs inherent in providing care there.

| More Savings Potential | Less Savings Potential | |

|---|---|---|

| Payments equalized to median prices at independent physician offices or ambulatory surgical centers, with no health system/hospital affiliation | Payments equalized to median prices at freestanding physician offices or ambulatory surgical centers, regardless of hospital/health system affiliation | Payments equalized to an amount between median prices at freestanding settings and HOPDs |

Payment Reference

Policymakers must determine how to translate their payment goals into specific payment amounts for each regulated service or set of services. They can do this either using a benchmarking approach or adopting a fee schedule:

- Public Benchmark: Under a benchmarking approach, policymakers could define reimbursement for site-neutral services as a multiple of an existing public fee schedule, such as Medicare or Medicaid rates. Using a multiple of Medicare rates—and the extensive data collection and analysis that undergirds them—may result in a significantly simpler payment methodology compared to other approaches. Policymakers would still need to address some complications, however, such as determining appropriate amounts for services that Medicare does not commonly cover and may inadequately reimburse. There also may be distinctions between how Medicare and commercial payers package services for payment that may need to be untangled.

- Private Market Benchmark: Privately negotiated prices—such as statewide median or average in-network rates—also could serve as a benchmark. This approach would require agreement on a common database to use, such as a state all-payer claims database or one of several commercial health databases. Policymakers should be attentive to potential limitations and distortions in available data, and explore adjustments that reflect and reinforce the underlying policy goals for site-neutral payment. For example, policymakers will need to determine which providers’ prices are included in calculating the benchmark, such as including all freestanding providers or only independent providers.

- Fee Schedule: A de novo fee schedule approach, in contrast, would require authorities to determine the appropriate reimbursement level for each individual service or group of similar services (such as Medicare’s Ambulatory Payment Classifications) from scratch. This would likely be significantly more time-consuming and labor intensive than picking a benchmark based on existing programs or pricing distributions. It could also invite heightened debate over the appropriateness of the amount chosen for each service or group of services.

| Less Analytically Complex | More Analytically Complex | |

|---|---|---|

| Benchmark based on existing public fee schedule | Benchmark based on commercial pricing data | New commercial fee schedule |

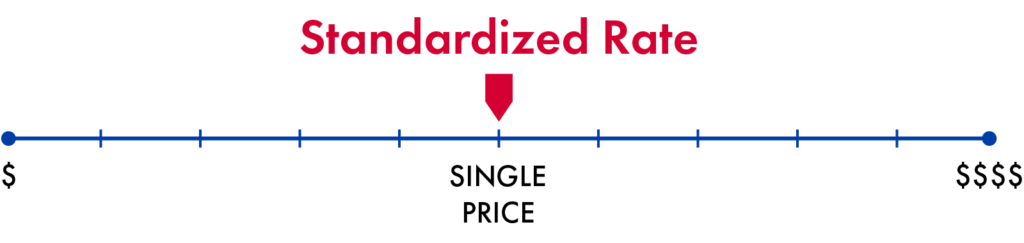

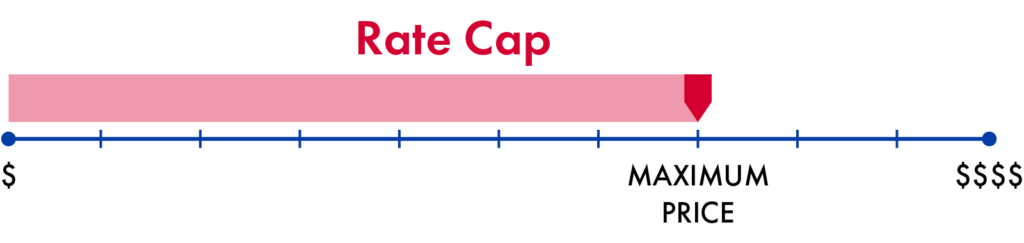

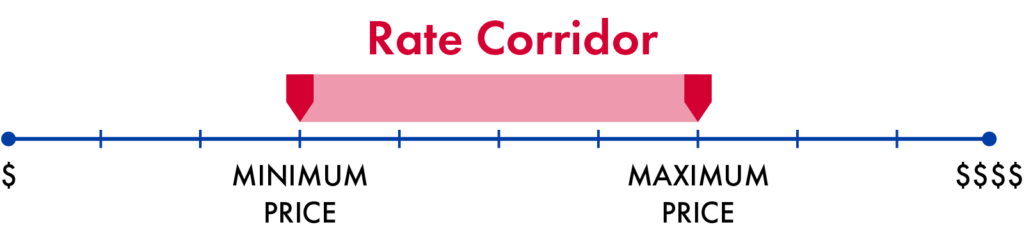

Payment Flexibility

A commercial site-neutral payment policy can leave more or less room for private negotiation to continue to play a role in prices, depending on its form.

Policymakers must determine which approach to adopt. Possible forms include:

- Standardized Rate: Policymakers could set standardized rates for services or groups of services, thus eliminating the role of market pricing for services covered by the policy. Every regulated hospital or health system, outpatient facility, and physician office would be paid the same rate (or base rate, if the methodology includes provider-level adjustments) as all other providers offering the service, regardless of their negotiating power.

- Rate Cap: Alternatively, policymakers could include a greater role for market pricing by capping provider payment rates while allowing for price negotiations between providers and payers below that limit.

- Rate Corridor: To address concerns that some providers are underpaid in the current market, policymakers could adopt a middle ground approach, such as a rate corridor with upper and lower payment limits (e.g., requiring payments fall between 100% and 150% of Medicare’s Physician Fee Schedule rate for the same service). This would ensure that private negotiations do not lead to inadequate reimbursement. Depending on local market dynamics, the upper payment limit of a rate corridor or cap may or may not become a de facto payment rate.

Payment Adjustments

Whatever way a payment limitation is structured, policymakers must decide to either use the same amount for all providers or specify provider-level adjustments similar to some Medicare payment systems. With a provider-level adjustment approach, reimbursement may not be strictly site-neutral, but differences in payment would reflect policy preferences rather than provider market power. This may provide a mechanism for softening the policy’s effects on certain hospitals, without exempting them from site-neutral payment altogether.

- Same Amount: All providers that fall within the scope of the policy would receive the same payment amount.

- Provider-Level Adjustments: These adjustments could allow for variation based on factors such as geography and/or area wage index, uncompensated care levels, payer mix, or other demonstrable cost differences. For example, policymakers could allow for higher payments to hospitals located in rural areas. To the extent policymakers use Medicare’s OPPS or physician fee schedule as a benchmark, they could allow Medicare’s geographic adjustments to automatically carry through. Other modifications, such as enhanced payments for safety-net or teaching hospitals, would need to be added on separately.

| Less Accommodating | More Accommodating | |

|---|---|---|

| No provider-level adjustments | Adjustments for geographic location and/or uncompensated care levels | Other adjustments based on policy priorities |

Phase-In Options

Policymakers will need to decide whether to implement a commercial site-neutral payment policy to immediately achieve their payment goal, or phase in to the ultimate goal over time. A faster implementation process will yield greater savings, while a slower phase-in will help providers adjust to the new payment policy.

Possible phase-in approaches:

- Reduce Payments over Time: Set the initial payment amount at the current median or mean in-network rate across settings, including higher-price HOPDs. Over a set number of years, the payment amount could be scheduled to fall to a level equal to the mean or median in-network rates in all freestanding or just independently owned settings. A similar approach would be to multiply the ultimate policy—for example, median prices in independent settings—by a defined percentage, which would decrease each year until the payment amount is equal to the final goal.

- Start with a Threshold: Policymakers also could begin with a rate cap or corridor and transition to standardized rates over time. This would allow for the gradual elimination of site-of-service differences without suddenly decreasing or increasing some providers’ reimbursement levels.

Annual Updates

Once prices are site-neutral, policymakers must determine the methodology for annual updates. This can provide an additional opportunity for savings.

Possible benchmarks could include:

- Medicare Rates: If policymakers benchmark payment amounts to a multiple of Medicare’s payment rate, year-to-year growth could naturally be tied to changes in Medicare’s rates. This could result in future year savings if Medicare rates grow more slowly than commercial payments.

- Consumer Price Indices: Indices such as growth in the consumer price index (CPI), CPI plus a modest increment (e.g., CPI+.5), or medical CPI, could also be used to annually update payment amounts, with policymakers choosing update factors based on year-to-year changes or averages over time for these indices.

Figure 8.

Potential Annual Update Growth Targets: Consumer Price, Medical Consumer Price, and Medicare Economic Indices and Trendlines, 2015-2025

Sources: U.S. Bureau of Labor Statistics, “Consumer Price Index,” 2025 U.S. Bureau of Labor Statistics “Consumer Price Index for All Urban Consumers: Medical Care in U.S. City Average,” 2025 Centers for Medicare & Medicaid Services, “Market Basket Data,” 2025

Operations

Policymakers will need to make other critical operational decisions that will shape the policy’s effect, including whom to regulate and how they should bill.

Whom to Regulate?

A commercial site-neutral payment policy could regulate the amount health care providers can charge and how they bill those charges, the amounts commercial payers reimburse for care, or both:

- Providers: A policy regulating providers could specify or limit the amount health care providers can bill or collect for services covered by commercial payers, regardless of the type of commercial insurance a patient has. A provider policy can also apply to—and therefore protect—care for self-pay patients who are uninsured, have gone out-of-network, or receive a service that is not covered by their health insurance policy.

- Payers: A policy regulating commercial payers could either specify or limit the amount commercial payers can reimburse providers for specified services or simply require that the payers’ rates be site-neutral at amounts they determine (with the risk that prices increase due to demands from market-dominant hospitals). A payer policy may not necessarily reach the whole commercial market. State policymakers cannot regulate self-insured group health plans subject to ERISA (which cover more than half of enrollees in employer-sponsored plans), and even comprehensive federal health insurance laws like the Affordable Care Act frequently exempt certain types of limited benefit or other alternative coverage options. A payer policy also would leave uninsured and other self-pay patients at risk of being responsible for higher, non-site-neutral amounts (perhaps more than before).

- Both: Regulating commercial payers in addition to providers may enhance oversight and enforcement, however. State insurance regulators could tap current health insurance rate review processes and market conduct exams to monitor reimbursement levels. A policy that regulates both providers and payers also could improve compliance, as both of the principal parties to a transaction would be responsible for complying with site-neutral requirements and potentially hold each other in check.

| Regulated Entity | Apply Across Commercial Market, Regardless of Plan Type | Protects Uninsured and Other Self-Pay Patients | State Insurance Oversight and Enforcement Tools Available |

|---|---|---|---|

| Providers |  | |  |

| Payers | | | |

| Providers & Payers | | | |

Targeted Payer Reforms

Policymakers who want to start slow could decide to apply site-neutral payment to a narrow range of payers, such as state employee health plans or qualified health plans offered on health insurance marketplaces. In some states, this approach could allow implementation of site-neutral payment without legislative action. Policymakers could also decide to start with a narrower range of payers and gradually phase-in site-neutral payment across markets.

Network Rules

Policymakers should strongly consider clearly specifying that commercial site-neutral payment requirements apply to care delivered by both in- and out-of-network providers.

- Drawbacks of an In-Network Only Approach: Applying site-neutral payment to only in-network care would likely encourage providers to leave payor networks. This, in turn, would create significant financial burdens for consumers, who often face higher out-of-pocket costs for out-of-network care, and limit the savings potential of these payment policy reforms.

- Limitations of an Out-of-Network Only Approach: Applying site-neutral payment to only out-of-network care would not have the same drawbacks as an in-network only approach and may encourage more providers to join payor networks. It would generate far lower savings, however.

Billing Rules

Policymakers may want to clearly specify how site-neutral payments should be billed:

- Split Billing: A commercial site-neutral payment policy could continue to permit split billing for services subject to site-neutral payment, as long as the total amount billed and paid for the combined facility and professional fees equals the amount paid to an independent professional. This approach presents some logistical challenges, particularly for out-of-network care where reimbursement rates are not negotiated in advance. Enforcement also may present significant challenges, as evaluating compliance would require consistently matching all claims submitted for a single service and ensuring the total amount is no higher than specified. If it is, payers will need a process for determining from whom overpayments are recovered. Continuing to allow split-billing also may expose some consumers to extra cost-sharing obligations related to separate facility and professional bills for a single service when care is provided at a hospital outpatient department.

- Unified Bill: Alternatively, commercial site-neutral payment rules could require providers to issue a unified bill for services covered by site-neutral rate requirements. This bill may come from the hospital or health care professional depending on the circumstances. A unified billing approach can protect consumers from extra out-of-pocket costs. It also is simpler for consumers receiving a bill or explanation of benefits, for payers negotiating rates and paying claims, and regulators monitoring compliance. This approach may have its own implementation challenges. Under a unified billing approach, providers would be expected to allocate revenue internally between the hospital and the professional. This may be more or less straight forward depending on their existing relationship. Policymakers may want or need to specify that any revenue shared by the billing professional with the hospital operating the HOPD where care was provided is exempt from any state-level fee-splitting prohibitions. Policymakers also may want to put in place guardrails to ensure allocations are reasonable and non-exploitative.

Can Health Care Be Like Buying a Plane Ticket?

When purchasing a plane ticket, consumers do not face separate bills from the airline and the airport. The airline collects a single payment from the consumer that covers both the airline’s expenses and various airline overhead costs, including landing fees, passenger fees, terminal fees, and usage fees. The airline is responsible for charging the appropriate airport charges as part of its ticket price and transmitting this revenue to the airport.

Location Identifiers

To implement, monitor, and enforce commercial site-neutral payment rules, payers and regulators need to distinguish the location of care on claims or in claims data. For example, depending on the policy, payment amounts for a particular service may depend on whether it is provided at an on- or off-campus HOPD. This often is not feasible in commercial claims.

Policymakers may want to specify how to include location information on claims. Options include:

- Setting Codes or Modifiers: Requiring that providers include codes or modifiers that distinguish when care is provided at an on- or off-campus HOPD or an independent setting, consistent with Medicare billing requirements. This approach provides less information to payers and regulators but may be easier to implement.

- Unique NPI: Requiring off-campus HOPDs to acquire a unique national provider identifier (NPI) and use this NPI on all commercial claims. Unique NPI requirements have been enacted in a few states and for the Medicare program beginning in 2028. States that pursue this approach should establish a system to associate each NPI with its affiliated hospital and health system to maximize transparency and data utility.

- Unique Suffix on Hospital NPI: Requiring off-campus HOPDs to attach a unique suffix to the main hospital campus’ NPI to distinguish separate locations. This approach would directly convey both the HOPD’s geographic location and information on the HOPD’s hospital or health system affiliation on the claim form, negating the need for a separate system.

| Less Information | More Information | |

|---|---|---|

| Setting codes or modifiers | Unique NPI | Unique suffix on hospital NPI |

Administration

Policymakers must make critical administrative decisions, including decision-making authority, monitoring and enforcement, that will impact the implementation process.

Decision-Making

Policymakers must determine whether and to what level of detail they define a commercial site neutral payment policy’s scope of services, settings, and payment method in statute, versus delegating some or all of these decisions to regulatory bodies.

If legislators choose to delegate these decisions, they will also need to identify which entity is charged with making these decisions (e.g., a new or existing administrative agency or independent commission) and determine the degree of autonomy and flexibility this entity wields as well as its funding levels, staffing, stakeholder engagement, and decision-making procedures, all of which will influence policy outcomes.

The most appropriate implementing agency will vary depending on the jurisdiction, existing authorities, and governing norms. State hospital rate setting experiences and recent experiences with state health care cost commissions and affordability offices may offer some lessons on the risks and opportunities inherent to tapping existing agencies versus establishing new agencies and independent commissions. To minimize regulatory capture, some features to consider include establishing funding independent of budget appropriations (such as through user fees), employing an expert and professional staff, and strictly following Administrative Procedures Acts.

Monitoring

Post-implementation reporting and monitoring will be a critical determinant of a commercial site-neutral payment policy’s ability to achieve cost savings without unintended side effects.

Policymakers will want to consider monitoring efforts that draw on data from providers and payers, including hospital financial information, negotiated rates, and commercial payer expenditures. Regulated entities should report information no less than annually, and agency officials should analyze and publicly release this information both in raw and processed forms.

To inform appropriate policy adjustments, analysts should regularly evaluate the policy’s impact on patient access and care quality, utilization, prices of non-site-neutral services, and providers’ financial health. Should the volume of certain services increase or decrease significantly, this could be a signal that particular prices have been set either too high or too low. Policymakers and managers will want to collect and monitor data that illuminates the access implications of these reforms and create mechanisms for adjusting rates if needed. In doing so, they may want to supplement data from claims repositories and provider reporting with patient and clinician surveys. MedPAC’s work monitoring the Medicare program could serve as a model.

Regulators or outside evaluators should share regular monitoring reports with policymakers and make them publicly available. In addition to informing policymakers overseeing the program, these assessments could inform policymakers in other jurisdictions considering site-neutral payment reforms.

Enforcement

Policymakers will need to consider including enforcement mechanisms for instances of non-compliance with a commercial site-neutral payment policy. This could include:

- Financial penalties: The implementing agency could be given authority to impose financial penalties on providers and/or payers and require these regulated entities to create and implement remediation plans, which would in turn receive extra monitoring. If so, penalty amounts should be high enough relative to the reductions in revenue from the policy to ensure regulated entities comply.

- Liability: State policymakers could also provide that a violation of the site-neutral billing requirements constitutes a violation of their state’s Unfair and Deceptive Practices Act. Depending on state law, this approach could allow for enforcement by the state attorney general, as well as private enforcement actions by consumers.

- Records Subpoena: To the extent a policy regulates what insurers and/or third-party administrators can reimburse for covered services, it could authorize the agency overseeing these entities to demand and inspect all relevant records from and impose penalties on those insurers or administrators that enter into contracts or make reimbursements that exceed the specified site-neutral payment amounts.

- Rate Reviews: The agency also could be authorized to disapprove health insurance premiums if an insurer cannot show that they have implemented site-neutral payments.

Policymakers could also seek to leverage patients, insurers, and/or third-party administrators in enforcement by creating mechanisms by which they can report non-compliant health care providers and, potentially, incentives for reporting.

Ready to Draft Legislation?

For additional guidance, the National Academy of State Health Policy (NASHP) has released model legislation to establish site-neutral commercial payment for select outpatient health care services.

About

Authors: Christine H. Monahan, Karen Davenport, Julia Burleson, and Kennah Watts

Published April 2026

This work was completed in partnership with West Health. Related research and resources on outpatient facility fee billing is available here.